Part 5 of 7 in the Capital Raising Series | Veritas Global Law PLLC

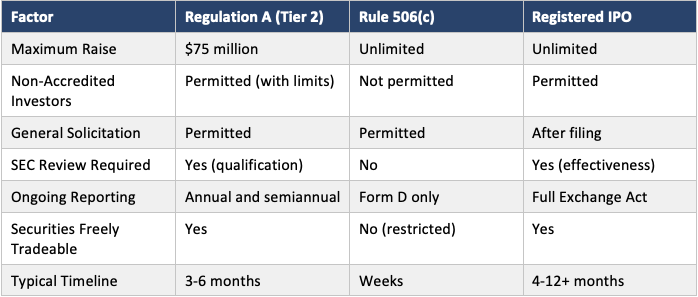

Between the private world of Regulation D and the fully public realm of registered offerings lies Regulation A—an exemption that offers a middle path for companies seeking significant capital without the full burden of going public. Often called a “mini-IPO,” Regulation A allows issuers to raise up to $75 million annually while selling securities to both accredited and non-accredited investors.

The exemption underwent a substantial transformation in 2015 when the SEC implemented Regulation A+ as mandated by the JOBS Act, dramatically expanding offering limits and creating a two-tier structure that provides meaningful flexibility. Subsequent amendments in 2018 and 2020 further refined the framework, making Regulation A an increasingly viable option for companies seeking public capital without full SEC registration.

This article examines Regulation A comprehensively—the distinction between Tier 1 and Tier 2 offerings, the SEC qualification process, ongoing reporting obligations, and the strategic considerations that determine whether this exemption fits your capital-raising objectives.

Understanding the Two-Tier Structure

Regulation A offers two distinct pathways, each with different offering limits, compliance requirements, and regulatory characteristics. Choosing between Tier 1 and Tier 2 significantly shapes your offering structure and ongoing obligations.

Tier 1: Smaller Offerings with State Oversight

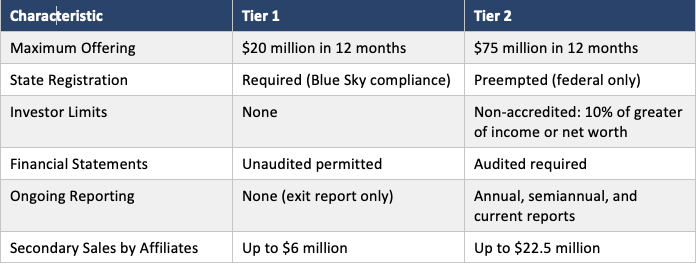

Tier 1 permits offerings of up to $20 million in a 12-month period, including up to $6 million in secondary sales by selling securityholders who are affiliates of the issuer. This tier preserves state authority over offerings, requiring compliance with Blue Sky laws in each state where securities are offered or sold.

State Registration Requirements

Unlike Rule 506 offerings—which enjoy federal preemption from state registration—Tier 1 offerings must navigate state securities laws. This creates meaningful complexity for offerings targeting investors across multiple jurisdictions.

To address this challenge, NASAA (the North American Securities Administrators Association) developed a coordinated review program for Regulation A offerings. Under this program, one state serves as lead examiner, coordinating with other participating states to streamline the review process. While helpful, this coordination does not eliminate state-level requirements or the need for state filings and fees.

Disclosure Requirements

Tier 1 issuers must file an offering statement on Form 1-A with the SEC, including:

• Part I: Notification providing basic information about the issuer and the offering

• Part II: Offering circular containing narrative disclosure about the business, risk factors, use of proceeds, management, and financial condition

• Part III: Exhibits including organizational documents, material contracts, and other specified items

A significant advantage of Tier 1: financial statements may be unaudited. This reduces both cost and preparation time compared to Tier 2’s audit requirement, making Tier 1 more accessible for smaller companies without established audit relationships.

Post-Qualification Obligations

Tier 1 imposes minimal ongoing obligations after the offering concludes. Issuers must file a Form 1-Z exit report within 30 calendar days after the termination or completion of the offering, reporting final offering results. No ongoing periodic reporting is required—a significant advantage for companies that prefer to avoid public company-style obligations.

Tier 2: Larger Offerings with Federal Preemption

Tier 2 permits offerings of up to $75 million in a 12-month period, including up to $22.5 million in secondary sales by affiliate selling securityholders. The higher ceiling and federal preemption from state registration make Tier 2 attractive for companies seeking substantial capital from geographically diverse investors.

Federal Preemption: A Major Advantage

Securities sold in Tier 2 offerings are “covered securities” under the National Securities Markets Improvement Act, meaning state registration requirements do not apply. States may require notice filings and collect fees, but they cannot impose substantive registration conditions or merit review. For offerings targeting investors across many states, this preemption provides substantial practical benefits.

Investment Limits for Non-Accredited Investors

Unlike Tier 1, Tier 2 imposes investment limits on non-accredited natural person investors. These investors cannot purchase securities in a Tier 2 offering in an amount exceeding 10% of the greater of their annual income or net worth (for natural persons) or 10% of the greater of annual revenue or net assets (for entities).

This limitation does not apply to accredited investors, who face no investment cap. The practical effect: issuers must collect information about investor qualification and, for non-accredited investors, about income and net worth to verify compliance with investment limits.

Audited Financial Statement Requirement

Tier 2 offerings require audited financial statements prepared in accordance with U.S. GAAP and audited by an independent public accountant. The audit requirement adds cost and extends preparation timelines but provides investors with greater assurance regarding financial information accuracy.

Financial statements must cover the two most recently completed fiscal years (or the period since inception for newer companies). Interim financial statements are required if the most recent fiscal year ended more than nine months before the qualification date.

Ongoing Reporting Obligations

Tier 2 issuers assume ongoing reporting obligations that resemble—though are less burdensome than—public company reporting:

• Annual Reports on Form 1-K: Due within 120 calendar days after fiscal year end, containing audited financial statements and updated business disclosure

• Semiannual Reports on Form 1-SA: Due within 90 calendar days after the end of the first six months of the fiscal year, containing unaudited interim financial statements

• Current Reports on Form 1-U: Required for specified material events, including fundamental changes, bankruptcy, changes in accountants, and departure of certain officers

• Exit Report on Form 1-Z: Filed when the issuer terminates its Regulation A reporting obligations

These obligations continue until the issuer becomes subject to Exchange Act reporting, the issuer or another party purchases or repurchases all securities sold in Regulation A offerings, or the issuer files an exit report after meeting specified conditions.

The SEC Qualification Process

Unlike Regulation D exemptions—where issuers file a notice after the first sale—Regulation A requires SEC review and qualification of an offering statement before sales can begin. This process more closely resembles traditional registered offerings, though with somewhat lighter requirements.

Filing and Review Timeline

The qualification process typically proceeds as follows:

• Initial Filing: The issuer files Form 1-A with the SEC, either publicly or confidentially. Confidential submission allows issuers to receive SEC comments without public disclosure of the draft offering statement.

• SEC Review: The Division of Corporation Finance reviews the filing and typically issues comment letters identifying questions or requesting revisions. Review timing varies based on SEC workload but commonly takes several weeks to several months.

• Response and Amendment: The issuer responds to SEC comments and files amended offering statements as needed. Multiple rounds of comments may occur.

• Qualification: Once the SEC staff completes its review and is satisfied with the disclosure, it issues a qualification notice. Sales may commence only after qualification.

Testing the Waters

Regulation A permits issuers to “test the waters” by soliciting non-binding indications of interest from potential investors before or during the SEC review process. This allows companies to gauge market interest before incurring full qualification costs.

Testing the waters materials must be filed with the SEC but may be used to communicate with potential investors and obtain indications of interest. No sales or commitments can occur until qualification, but the ability to build investor interest during the review period provides meaningful flexibility.

Bad Actor Disqualification Under Regulation A

Regulation A incorporates bad actor disqualification provisions that prevent certain individuals and entities with problematic regulatory histories from using the exemption. These provisions mirror those applicable to Regulation D and require careful attention during offering planning.

Covered Persons

The disqualification provisions apply to:

• The issuer, including predecessors and affiliated issuers

• Directors, officers, general partners, and managing members of the issuer

• Beneficial owners of 20% or more of the issuer’s outstanding voting equity

• Promoters connected with the issuer

• Underwriters and their directors, officers, and partners

• Persons compensated for soliciting investors and their associated persons

Disqualifying Events

Disqualifying events include criminal convictions, court injunctions, regulatory orders, SEC disciplinary actions, and other specified events related to securities violations. The lookback periods vary by event type—typically five to ten years—and the consequences depend on when the event occurred relative to the rule’s effective date.

Issuers must conduct thorough bad actor inquiries covering all covered persons before filing the offering statement. Discovering a disqualifying event after filing—or worse, after qualification—creates significant remediation challenges. The SEC may refuse to qualify an offering if disqualifying events exist and no waiver has been obtained.

Waiver Process

The SEC may grant waivers from disqualification upon a showing of good cause. The waiver process requires a written application explaining the circumstances and why disqualification is not necessary for investor protection. Waivers are discretionary and not automatic—issuers should not assume a waiver will be granted.

Regulation A+ and Subsequent Amendments

The 2015 Regulation A+ amendments transformed what had been a little-used exemption into a viable capital-raising pathway. Subsequent amendments have continued to refine and expand the framework.

Key 2015 Changes (Regulation A+)

• Created the two-tier structure with expanded offering limits

• Established federal preemption for Tier 2 offerings

• Permitted testing the waters communications

• Allowed confidential SEC review

• Modernized disclosure requirements

2018 Amendments

The 2018 amendments extended Regulation A eligibility to Exchange Act reporting companies, which had previously been excluded. This change allows public companies to use Regulation A as an alternative to registered offerings for raises within the applicable limits.

2020 Harmonization

The 2020 amendments harmonized various exempt offering rules and increased the Tier 2 maximum from $50 million to $75 million (and the Tier 1 maximum from $20 million, which was confirmed at this level). These changes expanded Regulation A’s utility for larger capital raises.

Strategic Considerations: When Regulation A Makes Sense

Regulation A occupies a distinctive position between private placements and registered public offerings. Understanding when this middle path serves your objectives requires considering several factors.

Advantages of Regulation A

• Non-Accredited Investor Access: Unlike Rule 506(c), Regulation A permits sales to non-accredited investors without requiring them to meet sophistication standards. This broadens the potential investor base significantly.

• General Solicitation Permitted: Issuers can market their offerings publicly, using advertising, social media, and other mass communications to reach potential investors.

• Freely Tradeable Securities: Securities sold in qualified Regulation A offerings are not “restricted securities” under SEC rules. Purchasers may resell without complying with Rule 144 holding periods.

• Pathway to Public Markets: Some issuers use Regulation A as a stepping stone toward broader public company status, building a shareholder base and trading history before pursuing exchange listing.

• Testing the Waters: The ability to gauge investor interest before full SEC review provides valuable market intelligence before committing substantial resources.

Considerations and Limitations

• Time and Cost: The SEC qualification process takes time—often several months—and requires substantial legal, accounting, and preparation costs. Regulation D offerings can proceed more quickly with lower upfront expenses.

• Ongoing Obligations: Tier 2’s reporting requirements create continuing compliance costs that may strain smaller company resources.

• Offering Limits: While $75 million is substantial, companies needing larger raises may find full registration or Rule 506 more appropriate.

• Market Reception: Not all investor communities are familiar with Regulation A offerings, potentially affecting investor interest compared to more established offering types.

Regulation A Compared to Alternatives

Common Use Cases for Regulation A

• Consumer Brands Seeking Customer-Investors: Companies with loyal customer bases can use Regulation A to offer equity to their communities, converting customers into stakeholders.

• Real Estate Offerings: REITs and real estate companies use Regulation A to access retail investors while avoiding full registered offering requirements.

• Community-Focused Businesses: Local businesses, breweries, restaurants, and similar enterprises use Regulation A to raise capital from their communities.

• Pre-IPO Companies: Some companies use Regulation A as a stepping stone, building public market experience before pursuing exchange listing.

• Secondary Trading Development: Companies seeking to develop trading markets for their securities may use Regulation A to create freely tradeable shares.

Looking Ahead

Regulation A continues to mature as an offering pathway. The exemption has seen increased usage since the 2015 amendments, though it remains less common than Regulation D offerings. For companies seeking to combine public solicitation with access to non-accredited investors—while maintaining lighter ongoing obligations than full public company status—Regulation A offers a distinctive value proposition.

The next article in this series examines Regulation Crowdfunding—the exemption that democratizes capital access by allowing companies to raise up to $5 million through SEC-registered intermediaries while accepting investments from the general public.

Take the Next Step

Evaluating whether Regulation A fits your capital-raising strategy requires understanding the SEC qualification process, comparing Tier 1 and Tier 2 requirements, and assessing whether the exemption’s characteristics align with your business objectives and investor base.

Schedule a consultation with Veritas Global today. Our securities attorneys can help you assess whether Regulation A serves your goals, prepare the offering statement for SEC review, and navigate the qualification process from filing through closing.

This article is for informational purposes only and does not constitute legal advice. Securities regulations are complex and fact-specific; consult qualified counsel before structuring any offering.