Part 4 of 7 in the Capital Raising Series | Veritas Global Law PLLC

When conversations turn to Regulation D, most practitioners immediately think of Rule 506. And for good reason—Rule 506’s unlimited offering size and federal preemption of state registration make it the go-to exemption for venture capital rounds, private equity transactions, and fund formations. But this focus on 506 has left Rule 504 underappreciated, despite offering genuine advantages for certain capital-raising scenarios.

Rule 504 permits offerings of up to $10 million in a 12-month period. That ceiling might seem modest compared to Rule 506’s unlimited potential, but for early-stage companies seeking seed funding, real estate syndications below the $10 million threshold, or small business expansions, Rule 504 provides a pathway worth serious consideration—particularly when combined with state law exemptions that can remove resale restrictions and even permit general solicitation.

This article examines Rule 504 comprehensively: its mechanics, its relationship with state securities laws, and the specific circumstances where it may offer advantages over its more prominent Regulation D siblings.

The Core Framework: What Rule 504 Provides

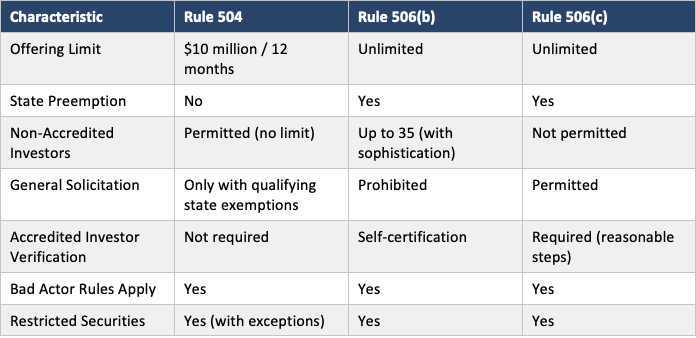

Rule 504 of Regulation D exempts from SEC registration the offer and sale of up to $10 million of securities within a 12-month period. Unlike Rules 506(b) and 506(c), Rule 504 does not impose federal restrictions on investor sophistication or accreditation—the exemption itself permits sales to any investor, regardless of financial status or investment experience.

This flexibility regarding investor qualifications comes with a significant trade-off: Rule 504 does not preempt state securities laws. While Rule 506 offerings are “covered securities” that bypass state registration requirements, Rule 504 offerings must comply with the securities laws of every state in which securities are offered or sold. This distinction fundamentally shapes how Rule 504 offerings are structured and marketed.

Key Characteristics of Rule 504

• Offering Limit: Up to $10 million in any 12-month period, calculated by aggregating all securities sold under Rule 504 during the measurement period

• Investor Requirements: No federal limitations on investor type—both accredited and non-accredited investors may participate without sophistication requirements

• General Solicitation: Generally prohibited, unless the offering qualifies under specific state law conditions (discussed below)

• State Law Compliance: Required in all states where securities are offered or sold—no federal preemption

• Form D Filing: Required within 15 days after the first sale of securities

• Resale Restrictions: Securities are “restricted” unless sold under specified conditions that remove this limitation

Who Can—and Cannot—Use Rule 504

Rule 504 includes specific eligibility restrictions that exclude certain categories of issuers. Understanding these limitations early in the planning process prevents wasted effort on an unavailable exemption.

Ineligible Issuers

The following companies cannot rely on Rule 504:

• Exchange Act Reporting Companies: Companies already subject to the periodic reporting requirements of the Securities Exchange Act of 1934 cannot use Rule 504. These companies must look to other exemptions or registered offerings for additional capital.

• Investment Companies: Entities registered or required to be registered under the Investment Company Act of 1940 are ineligible. This exclusion prevents registered mutual funds and similar vehicles from using Rule 504.

• Development Stage Companies Without Specific Business Plans: Companies that have no specific business plan or have indicated that their business plan involves engaging in a merger or acquisition with an unidentified company are excluded. This “blank check” prohibition addresses concerns about shell companies raising capital without clear business purposes.

• Companies Subject to Bad Actor Disqualification: Issuers with disqualifying events under Rule 504’s bad actor provisions cannot rely on this exemption. We address these provisions in detail below.

For most operating businesses—startups, small businesses seeking expansion capital, real estate ventures, and similar enterprises—these restrictions pose no obstacle. The eligibility requirements primarily screen out companies that raise specific investor protection concerns.

The $10 Million Calculation: Aggregation Rules

Rule 504’s $10 million limit applies to a rolling 12-month period. Calculating available capacity requires understanding what securities count toward this limit.

What Gets Aggregated

The $10 million ceiling includes the aggregate offering price of all securities sold under Rule 504 within the 12 months before the start of, and during, the current offering. This means an issuer must look backward 12 months from each new sale to determine remaining capacity.

Importantly, securities sold under other exemptions—such as Rule 506(b), Rule 506(c), or Regulation A—generally do not count against the Rule 504 limit. The SEC’s integration doctrine and safe harbors provide guidance on when offerings may be combined, but offerings that clearly rely on different exemptions with different requirements typically remain separate.

Practical Planning Considerations

For issuers planning multiple capital raises, the 12-month rolling window creates both constraints and opportunities. An issuer that raised $7 million under Rule 504 eleven months ago might have only $3 million in remaining capacity today—but will regain capacity as the earlier sales fall outside the measurement window.

Companies anticipating capital needs exceeding $10 million should consider whether Rule 504 is the appropriate vehicle, or whether Rule 506 (with its unlimited ceiling) better serves their objectives despite different compliance requirements.

State Securities Law Compliance: The Critical Variable

Unlike Rule 506 offerings—which preempt state registration under the National Securities Markets Improvement Act—Rule 504 offerings must navigate state securities laws in every jurisdiction where securities are offered or sold. This reality shapes offering strategy in fundamental ways.

Why State Compliance Matters

Each state maintains its own securities laws (often called “Blue Sky” laws) with distinct registration requirements, exemptions, and procedures. For a Rule 504 offering to investors in multiple states, the issuer must either register the offering in each state or qualify for a state-level exemption in each jurisdiction.

State registration can be time-consuming and expensive. “Merit Review” states may evaluate whether the offering terms are “fair, just, and equitable” to investors—a subjective standard that can result in required modifications to offering terms. Coordination among multiple states’ review processes adds complexity.

Common State Exemption Strategies

Most Rule 504 offerings rely on state exemptions rather than state registration. Common approaches include:

• Accredited Investor Exemptions: Many states provide exemptions for sales exclusively to accredited investors. These exemptions typically require notice filings and fees but avoid substantive state review.

• Limited Offering Exemptions: Some states exempt offerings to limited numbers of investors (often 25 or fewer per state) within specified time periods.

• Uniform Securities Act Exemptions: States that have adopted versions of the Uniform Securities Act may offer standardized exemption provisions.

• Small Corporate Offering Registration (SCOR): Certain states participate in the SCOR program, which provides coordinated registration procedures for smaller offerings.

The availability of state exemptions varies significantly by jurisdiction. Issuers should map their anticipated investor locations early in the planning process to identify which states require attention and what exemption strategies are available.

Resale Restrictions and Securities Status

Securities sold under Rule 504 are generally “restricted securities” under SEC rules. Restricted securities cannot be freely resold in public markets; instead, resales must comply with an exemption from registration (such as Rule 144) or occur pursuant to an effective registration statement.

This restriction affects investor expectations and liquidity. Purchasers in a Rule 504 offering should understand they may need to hold their investment for an extended period before any resale opportunity arises.

Exceptions: When Securities Are Not Restricted

Rule 504 provides important exceptions where securities are not restricted and may be freely resold. This occurs when the offering is made:

• Exclusively under state laws that require public filing and delivery of a disclosure document to investors before sale; or

• In states that require registration of the securities and public filing and delivery of a substantive disclosure document; or

• Exclusively according to state law exemptions that permit general solicitation, provided sales are made only to accredited investors.

These exceptions create meaningful structuring opportunities. An issuer willing to comply with state registration or specific state exemption requirements can offer securities that purchasers may freely resell—an advantage that may attract investors who value liquidity.

General Solicitation: Limited but Possible

Unlike Rule 506(c)—which explicitly permits general solicitation—Rule 504 generally prohibits general solicitation and advertising. However, an important exception exists: issuers may engage in general solicitation if the offering is made exclusively under state law exemptions that permit general solicitation and sales are made only to accredited investors.

This provision allows certain Rule 504 offerings to be publicly marketed, provided the state law conditions are satisfied. For issuers in states with favorable exemption structures, this can combine Rule 504’s flexibility with public marketing capabilities.

Practical Considerations for General Solicitation

Issuers contemplating general solicitation under Rule 504 should carefully map the state law landscape. Not all states permit general solicitation under their exemptions, and the conditions for permissible solicitation vary. Attempting general solicitation without satisfying state law requirements can compromise both the federal and state exemptions.

For many issuers, if general solicitation is essential to the capital-raising strategy, Rule 506(c) provides a more straightforward path—albeit with the requirement to verify accredited investor status. The choice between Rule 504 with state-dependent general solicitation and Rule 506(c) with mandatory verification depends on specific offering characteristics and investor relationships.

Bad Actor Disqualification: Protecting the Exemption

Rule 504 incorporates bad actor disqualification provisions that mirror those applicable to Rule 506 offerings. These rules prevent certain individuals and entities with problematic regulatory histories from participating in exempt offerings.

Covered Persons Under Rule 504

The bad actor inquiry extends to:

• The issuer, including predecessors and affiliated issuers

• Directors, executive officers, and other officers participating in the offering

• General partners and managing members of the issuer

• Beneficial owners of 20% or more of the issuer’s outstanding voting equity securities

• Promoters connected with the issuer in any capacity

• Persons compensated for soliciting investors, and their directors, executive officers, and general partners

Disqualifying Events

Disqualifying events include:

• Criminal convictions within the past ten years (five years for the issuer) related to securities, false filings, or financial institution conduct

• Court injunctions or restraining orders within the past five years related to securities activities

• Final orders from state securities regulators, banking regulators, insurance regulators, credit union regulators, federal banking agencies, or the NCUA barring association with regulated entities

• SEC disciplinary orders relating to brokers, dealers, investment advisers, or their associated persons

• SEC cease-and-desist orders related to scienter-based antifraud provisions or Section 5 registration requirements

• Suspension or expulsion from membership or association with an SRO

• U.S. Postal Service false representation orders within the past five years

Conducting the Bad Actor Inquiry

Issuers must take reasonable steps to determine whether any covered person has a disqualifying event. This typically involves distributing detailed questionnaires to all covered persons, conducting searches of SEC, FINRA, and state regulatory databases, and documenting the inquiry process and results.

If a disqualifying event occurred before September 23, 2013 (the effective date of the bad actor rules), the exemption remains available provided the event is disclosed to investors. Events occurring after that date disqualify the exemption unless the SEC grants a waiver for good cause shown.

The bad actor inquiry should occur early in the offering planning process. Discovering a disqualifying event after investors have been solicited creates difficult remediation challenges.

Form D Filing Requirements

Issuers relying on Rule 504 must file a Form D with the SEC no later than 15 calendar days after the first sale of securities. Form D is a notice filing—not an application for SEC approval—that provides basic information about the issuer, the offering, and the exemption claimed.

Key Filing Considerations

• Timing: The 15-day clock begins running from the first sale, meaning when the investor’s commitment becomes irrevocable and the issuer accepts it.

• Amendments: If information becomes inaccurate or materially changes, or if the offering continues more than one year, amendments are required.

• Public Availability: Form D filings are publicly accessible through SEC EDGAR, meaning competitors, journalists, and others can view basic offering information.

• Failure Consequences: While failing to file Form D does not automatically destroy the exemption, it can trigger SEC enforcement interest and affect state filing compliance.

Rule 504 vs. Other Regulation D Exemptions

Understanding how Rule 504 compares to Rules 506(b) and 506(c) helps identify when each exemption is most appropriate:

When Rule 504 Makes Strategic Sense

Rule 504 deserves consideration when specific circumstances align with its characteristics:

Smaller Raises Within a Single State or Limited States

For offerings concentrated in one state or a small number of states with favorable exemption structures, Rule 504’s lack of federal preemption matters less. The issuer must comply with state law regardless; the question is whether the federal exemption requirements favor Rule 504 or Rule 506.

Offerings to Non-Accredited Investors Without Disclosure Burden

Rule 506(b) permits non-accredited investors but requires substantial disclosure documents when they participate. Rule 504 imposes no such federal disclosure mandate. For issuers wanting to include friends-and-family investors who may not meet accredited thresholds, Rule 504 can reduce disclosure complexity—though state law requirements must still be satisfied.

Offerings Where Freely Tradeable Securities Add Value

If the issuer is willing to comply with state registration or specific state exemption requirements that result in unrestricted securities, the resulting liquidity may attract investors who would otherwise hesitate to commit capital to restricted securities with uncertain resale timelines.

Situations Where State Compliance Is Required Anyway

Some offerings involve regulatory requirements beyond federal securities law—state-specific investment limitations, industry licensing requirements, or other considerations—that require state-level engagement regardless of the federal exemption chosen. In these situations, Rule 504’s lack of federal preemption imposes no incremental burden.

Common Pitfalls and How to Avoid Them

• Underestimating State Compliance Complexity: The absence of federal preemption means state securities laws cannot be ignored or treated as an afterthought. Build state compliance into offering planning from the beginning.

• Miscalculating the $10 Million Limit: The rolling 12-month calculation can surprise issuers who don’t track prior Rule 504 sales carefully. Maintain clear records and calculate available capacity before marketing any offering.

• Assuming General Solicitation Is Available: General solicitation under Rule 504 requires specific state law conditions. Don’t assume public marketing is permitted without confirming state exemption requirements.

• Neglecting the Bad Actor Inquiry: Bad actor disqualification applies to Rule 504 just as it applies to Rule 506. Conduct thorough inquiries before commencing any offering activities.

• Failing to Consider Alternatives: Rule 504 has genuine advantages, but Rule 506 may be simpler for multi-state offerings. Evaluate exemption choices based on your specific circumstances rather than defaulting to any single approach.

Looking Ahead

Rule 504 occupies a valuable but specific niche in the capital formation landscape. Its $10 million ceiling, combined with state law compliance requirements, makes it best suited for smaller offerings with concentrated investor bases or specific structural objectives that align with its characteristics.

The next article in this series examines Regulation A—the “mini-IPO” exemption that provides a middle path between private placements and full public offerings, with the ability to raise up to $75 million while selling to both accredited and non-accredited investors.

Take the Next Step

Determining whether Rule 504 fits your capital-raising strategy requires careful analysis of your offering size, investor base, state law landscape, and structural objectives. The interplay between federal and state requirements creates both complexity and opportunity.

Schedule a consultation with Veritas Global today. Our securities attorneys can help you evaluate whether Rule 504 aligns with your objectives, navigate state compliance requirements, and structure an offering that meets both federal and state securities law standards.

This article is for informational purposes only and does not constitute legal advice. Securities regulations are complex and fact-specific; consult qualified counsel before structuring any offering.