The Landscape: Understanding Federal Securities Exemptions

Part 1 of 7 in the Capital Raising Series | Veritas Global Law PLLC

For startup founders, fund managers, and CFOs navigating the capital markets, one question emerges early in the fundraising process: how do you legally raise money from investors without going through the full SEC registration process?

The answer lies in securities exemptions—carefully designed pathways that allow companies to raise capital while providing appropriate investor protections. Understanding these exemptions isn’t just a regulatory checkbox; it’s a strategic decision that shapes your investor relationships, marketing approach, and long-term capital strategy.

This article provides the foundational framework you need before diving into specific exemptions. Whether you’re raising your first seed round or structuring a private investment fund, this overview will help you understand the landscape and identify which paths deserve deeper exploration.

Why Securities Registration Exists—And Why Exemptions Matter

The Securities Act of 1933 established a fundamental principle: before offering securities to the public, issuers must register with the SEC and provide detailed disclosures. This registration process protects investors by ensuring they have access to material information about the company, its management, and the risks involved.

However, full SEC registration is expensive, time-consuming, and often impractical for early-stage companies and private funds. The registration process can cost hundreds of thousands of dollars in legal and accounting fees, take months to complete, and trigger ongoing public reporting obligations that strain limited resources.

Congress and the SEC recognized that rigid registration requirements could stifle capital formation—particularly for smaller companies and private offerings where investors may be sophisticated enough to evaluate opportunities without the full panoply of public company disclosures. The result: a series of exemptions that allow private capital raising under defined conditions.

These exemptions aren’t loopholes. They’re intentional policy choices that balance investor protection with capital formation needs. Each exemption comes with its own requirements, limitations, and trade-offs. Choosing the right one requires understanding what each offers—and what it demands in return.

The Three Major Exemption Frameworks

Federal securities exemptions fall into three primary categories, each designed for different capital-raising scenarios:

Regulation D: The Private Placement Standard

Regulation D encompasses the most commonly used exemptions for private offerings. Within Regulation D, three rules provide distinct pathways:

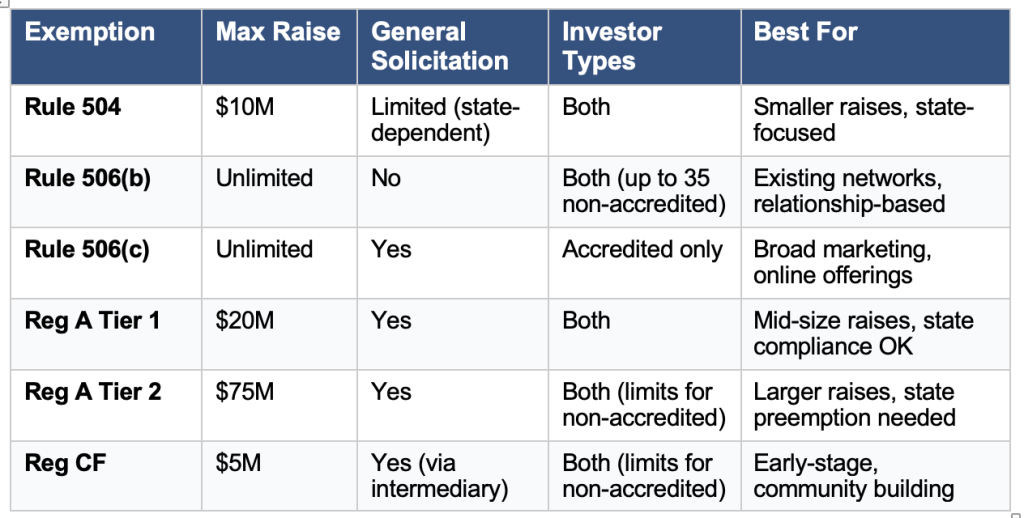

Rule 504 allows offerings up to $10 million within a 12-month period. It’s particularly useful for smaller raises and offers flexibility regarding investor types, though it relies heavily on state securities law compliance.

Rule 506(b) permits unlimited capital raising without general solicitation. Issuers can include up to 35 non-accredited investors (if they meet sophistication requirements), though doing so triggers additional disclosure obligations. Most 506(b) offerings limit participation to accredited investors to minimize compliance costs.

Rule 506(c) also permits unlimited raises but takes a different approach: it allows general solicitation and advertising, provided the issuer verifies that every investor is accredited. This verification requirement has historically been burdensome, though recent SEC guidance has simplified the process significantly.

Regulation A: The “Mini-IPO” Path

Regulation A provides a middle ground between private placements and full public offerings. It requires SEC qualification of an offering statement but allows issuers to raise capital from both accredited and non-accredited investors with fewer ongoing obligations than a registered public offering.

Tier 1 permits offerings up to $20 million in a 12-month period. Issuers must comply with state securities laws but face minimal ongoing reporting requirements after the offering.

Tier 2 raises the ceiling to $75 million and preempts state securities registration requirements—a significant advantage. However, Tier 2 issuers face ongoing reporting obligations, including annual, semi-annual, and current event reports.

Regulation Crowdfunding (Reg CF): Democratized Capital Formation

Regulation Crowdfunding (Reg CF) enables companies to raise up to $5 million in a 12-month period through SEC-registered intermediaries—either funding portals or broker-dealers. This exemption opened securities investing to the general public, with investment limits based on investor income and net worth for non-accredited participants.

Regulation CF requires specific disclosures through Form C filings and ongoing annual reporting. The intermediary requirement adds a layer of investor protection and standardization to the process.

Quick Comparison: Which Exemption Fits Your Scenario?

The following table provides a high-level comparison to help you identify which exemptions warrant deeper investigation:

Accredited vs. Non-Accredited Investors: A Critical Distinction

One of the most consequential decisions in structuring any offering is whether to include non-accredited investors. The SEC defines accredited investors based on income, net worth, or professional credentials. Individuals generally qualify if they have income exceeding $200,000 (or $300,000 with a spouse) in each of the past two years, or net worth exceeding $1 million excluding their primary residence.

Why does this matter? Including non-accredited investors typically triggers additional disclosure requirements designed to protect less sophisticated participants. Under Rule 506(b), for example, including even one non-accredited investor requires the issuer to provide financial statements and other disclosures similar to those required in registered offerings. These requirements add cost and complexity that many issuers prefer to avoid.

Most private placements therefore limit participation to accredited investors—not because non-accredited investors are prohibited, but because the cost-benefit analysis favors a streamlined process. Understanding this dynamic helps explain why many offerings you encounter will specify accredited-investor-only participation.

The Role of State Securities Laws

Federal exemptions don’t exist in isolation. State securities laws—often called “Blue Sky” laws—impose additional requirements that vary by jurisdiction. The interplay between federal and state requirements significantly affects exemption selection.

Rule 506 offerings (both 506(b) and 506(c)) benefit from federal preemption, meaning state registration requirements don’t apply, though notice filings may still be required. Regulation A Tier 2 offerings similarly preempt state registration. However, Rule 504, Regulation A Tier 1, and certain other structures require compliance with applicable state securities laws—a consideration that can significantly affect offering costs and timelines.

For issuers raising capital from investors across multiple states, federal preemption offers substantial practical advantages. This is one reason why Rule 506 remains the dominant choice for private placements despite other available options.

Bad Actor Disqualification: A Threshold Requirement

Before relying on Regulation D, Regulation A, or Regulation CF, issuers must consider the “bad actor” disqualification provisions. These rules prevent certain individuals and entities from participating in exempt offerings if they have relevant disciplinary history.

Covered persons include the issuer itself, directors, officers, general partners, managing members, promoters, and beneficial owners of 20% or more of voting equity. If any covered person has a disqualifying event—such as certain criminal convictions, regulatory orders, or court injunctions related to securities—the exemption may be unavailable.

Conducting a thorough bad actor inquiry early in the offering process is essential. Discovering a disqualifying event after marketing an offering creates significant problems. We’ll address specific bad actor requirements in detail within each exemption article in this series.

Strategic Considerations: Matching Exemptions to Objectives

Selecting an exemption isn’t purely a compliance exercise—it’s a strategic decision that affects your fundraising approach and investor relationships. Consider these factors:

Capital Requirements: How much do you need to raise? Rule 504’s $10 million cap and Regulation CF’s $5 million limit may be sufficient for early-stage companies, while larger raises require Regulation D Rule 506 or Regulation A.

Investor Base: Are you raising from an existing network of relationships, or do you need to reach new investors? The general solicitation rules under 506(b) and 506(c) create meaningfully different marketing constraints.

Investor Sophistication: Do your target investors meet accredited investor thresholds? If you want to include non-accredited investors, your exemption choices narrow and disclosure requirements increase.

Ongoing Obligations: Some exemptions trigger continuing reporting requirements. Regulation A Tier 2 and Regulation CF both require annual reports; Rule 506 offerings generally do not impose ongoing SEC filing obligations beyond the initial Form D.

Timeline: How quickly do you need capital? Regulation D offerings can proceed relatively quickly once documents are prepared, while Regulation A requires SEC review and qualification—a process that can take months.

Looking Ahead: This Series

This article provides the foundation; the following articles in this series will examine each exemption in depth:

Part 2: Rule 506(b) explores the most commonly used private placement exemption, including recent changes to disclosure requirements and strategies for structuring accredited-investor-only offerings.

Part 3: Rule 506(c) covers general solicitation offerings and the March 2025 SEC guidance that simplified accredited investor verification.

Part 4: Rule 504 examines offerings up to $10 million within a 12-month period, ideal for smaller raises and offerings with more flexible investor composition.

Part 5: Regulation A and Regulation A+ (Mini-IPO) covers the middle ground between private placements and full public offerings, with Tier 1 ($20M) and Tier 2 ($75M) offerings.

Part 6: Regulation Crowdfunding (Reg CF) details the intermediary-based model and investor protections built into SEC-registered funding portals for offerings up to $5 million.

Part 7: Strategic Comparison Guide provides a comprehensive framework for comparing all exemptions and selecting the right structure for your capital-raising objectives.

Take the Next Step

Understanding the securities exemption landscape is the first step toward structuring a compliant and effective capital raise. Each exemption involves nuanced requirements that deserve careful analysis based on your specific circumstances, investor relationships, and business objectives.

Schedule a consultation with Veritas Global today. Our team can help you evaluate which exemption aligns with your capital-raising strategy and guide you through the regulatory requirements from start to finish.

This article is for informational purposes only and does not constitute legal advice. Securities regulations are complex and fact-specific; consult qualified counsel before structuring any offering.